SUBMISSION TO THE SENATE ECONOMICS LEGISLATION COMMITTEE

Author: Cathal Leslie, Senior Economist, Prosper Australia

9 June, 2026

Summary of recommendations

Prosper Australia supports the Government’s stated objectives of improving housing affordability and intergenerational equity. However, we cannot support the proposed reforms. The package is poorly targeted and may prove counterproductive by increasing taxes on productive investment and younger Australians’ savings, while preserving significant advantages for property investors and failing to address untaxed land windfalls. Consistent with Prosper Australia’s longstanding research on housing, land taxation and economic rents, we consider that reform should instead reduce tax preferences for leveraged property investment and shift the tax burden away from productive activity and towards unearned gains from land.

Preferred reform package:

- Reject the proposed broad replacement of the CGT discount with inflation indexation. Retain the existing CGT framework for equities, businesses and other productive investments.

- Reduce the CGT discount for residential investment property from 50 per cent to 30 per cent. Existing investments should transition through a time-weighted discount rather than grandfathering.

- Phase out negative gearing for residential investment property over five years. The phase-out should apply to existing as well as future investments.

- Do not introduce a new-housing carve-out for either negative gearing or CGT. Such a concession would add complexity, create arbitrary boundaries and is likely to be capitalised into land and purchase prices rather than materially increase housing supply.

- Broaden the CGT base through deemed disposal at death. Death should generally trigger a CGT disposal at market value, subject to spousal rollovers and extended payment arrangements for genuinely illiquid estates. Trusts should be subject to periodic deemed-disposal rules.

- Capture planning-created land windfalls more directly. Introduce a development-pricing or land-uplift mechanism applying to gains attributable to rezoning and other planning decisions.

- Use the resulting revenue to reduce personal income-tax rates. This would shift the tax burden away from work and productive activity and towards economic rents.

If inflation indexation proceeds: - Provide more balanced treatment of capital gains and losses. Capital losses should either be indexed consistently with gains, as under the Chilean model, or capital gains should be subject to a lower capped rate, as in Israel and Mexico.

- Replace the proposed all-or-nothing residency test with proportional apportionment. Eligibility for indexation should reflect the proportion of an asset’s holding period during which the taxpayer was an Australian resident, broadly preserving the principle underlying the current CGT-discount rules.

- Limit delegated ministerial discretion over concessional asset classes. The assets eligible for preferential CGT treatment should be clearly defined in primary legislation rather than left open to expansion or alteration through ministerial instruments.

1. The economic rationale for these changes is flawed

As articulated in Treasury’s appearance at the recent Budget Estimates and Treasury Secretary Jenny Wilkinson’s speech to the Australian Business Economists1, the rationale for the proposed CGT and negative gearing changes appears to be based on four key premises:

- Inflation indexation is the only reasonable justification for relief, save for a narrow range of carve-outs where there are positive spillovers.

- Non-concessional rates on capital gains do not impact investment.

- Income shifting of labour income to capital gains is distortionary.

- Even if inflation indexation adds administrative complexity, it can be handled with new computing technology.

These premises are all questionable.

1.1 Concessional taxation of capital income

Besides potential carve-outs for small businesses and startups, the proposed inflation indexing aims to reduce the wedge between the tax treatment of capital income and other income sources. But the proposition that capital income should receive no differential treatment is not a dominant position in practice or in tax economics. Across the OECD, it is common to provide some form of relief for capital gains rather than tax the full nominal gain at ordinary personal income-tax rates.2 Countries do this through lower or capped rates, partial exemptions, holding-period concessions, inflation indexation, rollover relief and targeted treatment for assets or businesses.

These approaches reflect the fact that capital gains are not directly comparable with annual labour income: they may include inflation, accrue over many years, be realised in a single tax period, reflect profits already taxed at the company level, or reflect earned income that is saved from post-tax labour income. Relief is therefore not necessarily a concession in the ordinary sense; depending on its design, it may instead be required to measure real economic income more accurately and reduce distortions created by realisation-based taxation.

Similarly, Australia’s Future Tax System Review (the 2010 Henry Tax Review) recommended a 40 per cent discount, for a broad range of personal savings income, including capital gains and losses, interest and net rental income. Its objective was not simply to subsidise investors, but to reduce the distortion between consuming income immediately and saving it for future consumption. The UK’s Mirrlees Review (2010) went further, recommending that the normal return to saving should generally be exempt from tax, while excess returns above that allowance should be taxed under the same rate schedule as earned income. It reasoned that saving requires an individual to forgo current consumption and that the normal return represents the opportunity cost of doing so. Taxing that return can discourage saving, distort the allocation of capital between assets and, in an open economy, reduce domestic investment, productivity and wages.

These approaches do not necessarily support Australia’s blunt 50 per cent CGT discount. Both Henry and Mirrlees were concerned with constructing a coherent system. However, their conclusions demonstrate that the economic debate is not simply confined to inflation. Indeed, the OECD working paper cited by Jenny Wilkinson3 clearly states there is evidence for providing relief beyond inflation, including the double taxation of corporate profits. It also discusses the lumpiness of gains, under which income accumulated over many years may be taxed at an artificially high marginal rate when realised in a single year; the lock-in effect, under which realisation-based taxation discourages investors from reallocating assets; and the normal return to saving, which may be addressed through a rate-of-return allowance. The paper further acknowledges some evidence that CGT relief can support external investment in young firms.

It should also be stressed that measures designed to place capital and labour income on a comparable basis should not automatically be characterised as concessions. Wages are generally received and taxed annually, are not inflated by changes in the price level and have not borne an earlier layer of company tax. A realised capital gain may include many years of inflation; accumulated income pushed into a higher tax bracket by a single disposal and retained corporate profits that have already been taxed at the company level. Removing inflationary gains, averaging income across the period in which it accrued, or crediting corporate tax already paid does not necessarily favour capital over labour. These adjustments may instead be required to ensure that equivalent real economic income bears comparable tax. Likewise, capital gains do receive a genuine advantage from the deferral of tax until realisation, and any coherent comparison should recognise that benefit as well.

1.2 Double taxation of corporate profits hurts growth companies

The second premise underpinning the proposed CGT changes is that reducing the discount will have a minimal effect on investment. While it is encouraging that the government is consulting with the startup sector to assess how it will be affected by the proposed changes; the impact of higher CGT on investment is likely to be felt much more broadly across Australian firms.

Australia has a domestic dividend imputation system in which corporate income tax acts as a withholding tax for domestic shareowners. This largely nullifies the double taxation of corporate profits when disbursed as dividends for domestic shareholders. However, this is not the case where profits are retained within the firm, which is a practice that is frequently used by growing firms that wish to fund new investments. In these instances, shareholders receive their returns from share price growth, as retained profits are reinvested in the company. In effect, comparable tax treatment between shares and dividends requires some form of concession for capital gains.

OECD researchers4 have suggested that dividend imputation systems increase the relative size of future cashflow returns, which they argue could be priced into asset prices, thereby reducing the need for CGT relief on double taxation grounds. However, the case for this in Australia is weak. The Australian stock market is globally integrated and has a significant share of foreign ownership. Approximately a third of franking credits go unused (as they cannot be redeemed by foreign shareholders), rising to nearly half for listed equities,5 so it is unlikely that franking credits are fully priced into share prices. This is supported by UK evidence, where when dividend imputation was abolished for pension funds, local share prices did not meaningfully fall.6

In summary, retained earnings are especially important to younger, high-growth firms financing expansion and innovation. By contrast, large dividend payers are typically mature companies in concentrated sectors such as banking, mining, supermarkets and utilities. This approach risks redirecting investment away from businesses most likely to support innovation and productivity growth.

1.3 International competitiveness

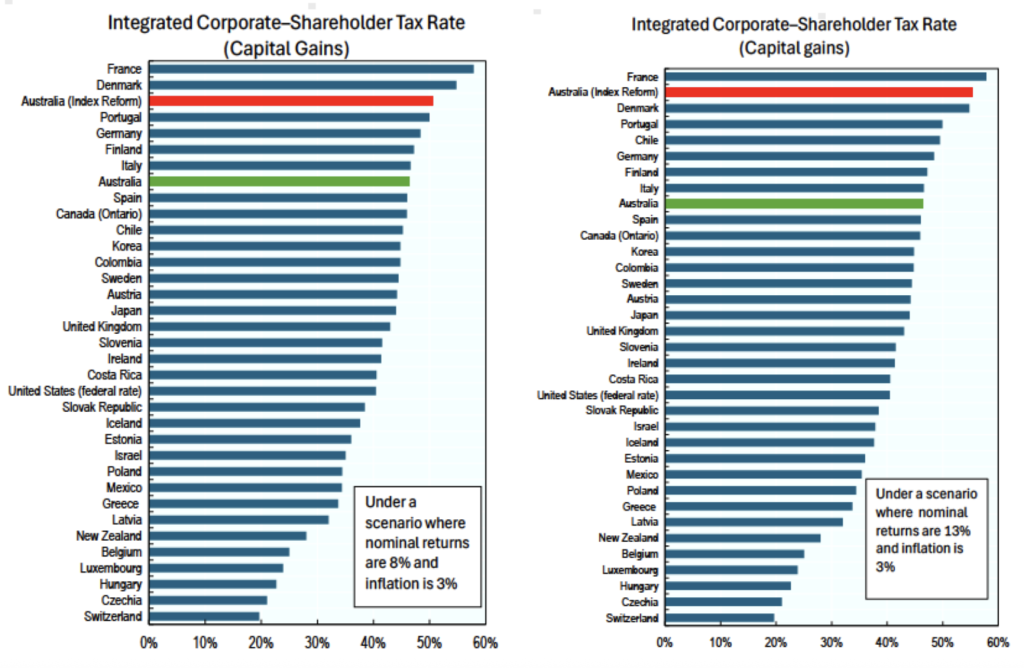

The disincentives for investing in innovative businesses are compounded by the internationally high rates of CGT incurred in Australia. This can be seen when comparing Australia’s integrated corporate–shareholder tax rate (or the total tax wedge on the underlying corporate profit) with international peers, which measures the compounded tax on capital income from corporate income tax and capital gains tax. Figure 1 estimates this rate for retained corporate earnings across OECD economies under two different return scenarios. Both assume an annual inflation of 3 per cent, approximately Australia’s average over the past decade. The first assumes a nominal return of 8 per cent, equivalent to a real return of approximately 5 per cent, while the second assumes a nominal return of 13 per cent, equivalent to a real return of approximately 10 per cent.

Even under Australia’s existing CGT discount, the combined tax rate on retained profits ranks poorly. Australia is in the top quarter of OECD countries under current tax settings. However, replacing the discount with inflation indexation would give Australia one of the highest combined tax burdens on retained corporate earnings for resident shareholders among the OECD countries modelled. Under standard modelling assumptions for a growth stock (in the scenarios detailed above), Australia would have the 2nd or 3rd highest corporate–shareholder tax rates in the OECD. Notably, it would also make us significantly harsher than other countries that use indexation (i.e. Israel, Chile and Mexico).

Retained earnings are an important source of finance for expanding firms. A higher integrated tax rate reduces the after-tax return available to shareholders when companies reinvest profits rather than distribute them as franked dividends. The reform would therefore strengthen the tax system’s existing bias in favour of dividend distributions and against the retention of earnings for investment, innovation and productivity growth.

Figure 1: Australia already has high capital income taxes by international standards, and inflation indexing would make things worse

Effective tax rate on retained earnings for a domestic shareholder

Note: the green bars represent Australia’s integrated corporate-shareholder tax rates for retained earnings under current GST settings, while the red bars present results of two inflation-indexed scenarios – a ‘moderate’ growth scenario (5% real returns) on the left and a ‘high’ growth scenario (10% real growth) on the right.

Source: Prosper Australia using OECD 2025 & PwC 2025

1.4 Concerns about income shifting between labour and capital gains are overstated

One reason advanced by OECD researchers7 to align the tax treatment of capital gains with labour income is concern about income-shifting to gain access to lower tax regimes, even where the income has primarily been derived from labour. However, there is little evidence that such income shifting occurs on a scale sufficient to justify an economy-wide increase in the taxation of capital gains.

Australian data do not allow a reliable estimate of how much labour income is recharacterised in this way, but the principal observable area of potential exposure is owner-managed businesses, where approximately $10 billion in annual gains may benefit from the small-business CGT concessions.8 These gains are difficult to disentangle into returns to labour and capital, as well as the gains that represent genuine risk-taking, property appreciation, business goodwill and entrepreneurial value.

While concerns about capital-labour income shifting may be well-founded, reducing CGT discounts to bring capital taxation more into line with labour taxation is not necessarily the most effective way forward. These issues could also be remedied through better tax administration. Indeed, Australian tax law already contains targeted mechanisms for addressing artificial attempts to convert labour income into more favourably taxed forms.

But crucially, the proposed CGT changes retain most small-business CGT concessions, even though owner-managed businesses are among the most plausible areas in which returns to labour and capital may be difficult to distinguish. If preventing the conversion of labour income into capital gains were a central objective, reform would begin with these identifiable concessions.

1.5 Other tax neutrality concerns are more pressing

At Budget Estimates and in the Treasury Secretary’s Australian Business Economists speech, she noted that the reform was motivated by tax neutrality: “decisions by individuals and businesses should be based on underlying economic merit, not tax treatment. Capital should flow to where it is most productive.”9 However, this argument is inconsistent with the new package. The new scheme replaces a flat CGT discount with a patchwork of inflation indexing for some assets and carve-outs for “new housing”. This is too narrow a view of tax neutrality, which should be considered across assets and saving vehicles.

The CGT changes will make investments held personally substantially less attractive relative to owner-occupied housing and superannuation. A personally held share or business asset may face tax on its indexed real gain at rates between 30 and 47 per cent. By contrast, gains on a taxpayer’s principal residence are entirely exempt, while a complying superannuation fund is generally taxed at 15 per cent during the accumulation phase and receives a one-third CGT discount on assets held for at least 12 months. The reform therefore, distorts incentives further to accumulate wealth through tax-favoured structures rather than underlying economic merit.

Superannuation is also not restricted to unleveraged portfolio saving. Self-managed superannuation funds may use limited recourse borrowing arrangements to acquire eligible assets, including investment property. The Government would therefore impose much higher tax rates on directly held investments while preserving access to leveraged investment within a substantially lower-taxed structure. This asymmetry is particularly difficult to justify given that the Financial System Inquiry recommended abolishing the limited-recourse borrowing exception, while the Council of Financial Regulators and ATO have identified its removal as a means of reducing risks to retirement savings, financial stability and property-price cycles.10

This is a more concrete tax-neutrality problem than the unquantified conversion of labour income into capital gains. A well-designed system should not cause the same underlying share, managed fund or property investment to face radically different tax rates merely because it is held personally, through superannuation or as a principal residence.

1.6 Inflation

The Treasury Secretary was right to identify inflation as a legitimate basis for providing relief from capital gains tax. Taxing the full nominal increase in an asset’s value can lead to incredibly punitive effective tax rates, particularly when inflation is high.

However, the proposed system applies indexation inconsistently. While inflation is recognised when calculating gains, losses are recognised only in nominal terms. An asset that has fallen substantially in real value may therefore generate no deductible loss, while a gain on another asset in the same portfolio remains largely taxable after indexation. This asymmetry distorts capital allocation by penalising risk-taking and discouraging investors from reallocating capital away from unsuccessful investments. It can also produce highly perverse outcomes: a taxpayer may face tax despite earning little or no net real return across their portfolio, and the effective tax rate on their net real income can readily exceed 100 per cent. Section 4 examines these loss-offsetting problems and their implications for investment in greater detail.

1.7 Simplicity is a virtue

Several OECD countries have moved away from inflation indexation and other highly technical methods of calculating capital gains. Australia replaced indexation with the CGT discount in 1999, the United Kingdom later abolished both indexation for individuals and its replacement, taper relief, and Ireland now limits indexation to historic expenditure. These reforms hint at a potential lesson: measures designed to calculate gains more precisely can impose substantial compliance costs and remain embedded in the tax system for decades.

Indexation is more complicated than adjusting the original purchase price by CPI. Separate cost-base items may have been incurred at different times, while share splits, reinvested dividends, capital improvements, partial disposals, inheritances, restructures and foreign-currency movements can all require additional calculations. Transitional rules add another layer, potentially requiring valuations or apportionment between old and new regimes. Complexity also grows when special rules are introduced for losses, temporary residents (see Section 5), startups and preferred asset classes. These changes will increase the need for professional advice.

Despite this burden, indexation corrects only one imperfection: the taxation of inflationary gains. It does not resolve lock-in, the lumpiness of realised gains, double taxation of retained corporate profits, the deferral advantage or asymmetric loss treatment. And frankly it is arguably not worth trying to design an academically pure capital gains tax regime, no country has or likely will be able to design a system that manages to tick off all the different issues.

The existing discount may be blunt, but it is transparent and comparatively simple.

2. Social mobility will be stifled by these changes

In addition to the stated economic rationale for changing CGT arrangements, the Government’s proposal has been argued to promote intergenerational equity. Unfortunately, the design of the tax changes will likely worsen inequality.

2.1 Young people will face a significant hike on the investments they can access

Young Australians are substantial participants in investment markets. The 2023 ASX Australian Investor Study suggests that roughly two in five Australians aged 18–24 held investments outside their home and superannuation, including around one in six who directly owned Australian shares.11

This participation is likely to continue to grow. Young people are now routinely exposed to investing through financial influencers and other social-media content, while low-cost brokerage platforms and exchange-traded funds have made it easier to begin investing with relatively small amounts. This is unlike property, which generally requires a large deposit and significant borrowing capacity, and hence is less accessible to young people.

Australia’s move from the 50 per cent CGT discount to inflation indexation is therefore not simply a tax increase on wealthy or older property investors; it will also increase the tax imposed on the long-term savings of a large and growing cohort of younger Australians, particularly where their investments earn returns materially above inflation.

2.2. The grandfathering of negative gearing entrenches intergenerational inequality

Grandfathering negative gearing is a deeply regressive and inefficient tax preference. Under the proposed arrangements, existing investors will continue to receive a tax advantage simply because they entered the market earlier, while younger and future investors would face a less favourable tax system. Similarly, someone who owns an owner-occupied residence, will still be eligible for negative gearing on that property if they decide to leave the property and rent it out.

The Treasurer notes that properties are negatively geared for an average of 5-10 years.12 This timing reflects behaviour under the current tax system and should not be treated as a fixed limit on the cost of grandfathering. Once access to negative gearing is restricted to existing properties, investors will have a stronger incentive to preserve and extend those deductible losses. They may postpone debt repayment, refinance or restructure borrowings, and delay expenditure that would return the property to positive taxable income. The grandfathered benefit could therefore persist for substantially longer than historical averages suggest, increasing both the fiscal cost and the inequity between existing and future investors.

A better approach would be a time-limited transition. For example, negative gearing benefits for existing assets could be phased down over a fixed period. That would give investors time to adjust while avoiding the inequity and inefficiency of permanently preserving a tax preference for one cohort of asset owners.

2.3 Increasing CGT hurts the middle class, not centi-millionaires or billionaires

A realisation-based CGT does not tax people according to their capital gains. It taxes people when they sell. Taxpayers who need liquidity realise gains. Those with the greatest wealth often do not. A middle-income investor may realise a gain because they need to fund retirement, move for work, separate from a partner, repay debt, or rebalance a modest portfolio. A very wealthy taxpayer can often defer, borrow against assets, or wait until death to bequeath their assets. The proposed model increases the tax burden on the act of realisation while leaving the deeper problem of indefinitely deferred gains untouched.

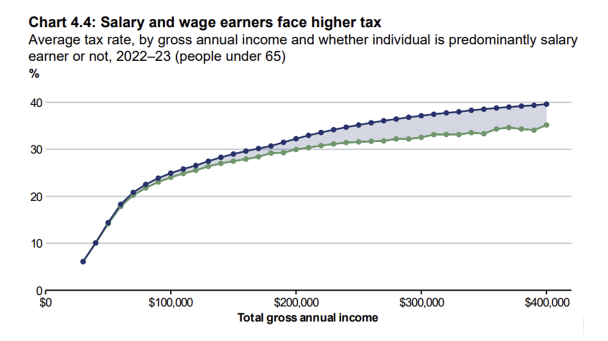

This is why the CGT reforms will miss the very top of the wealth distribution – a limitation evident in Treasury’s Budget Chart 4.4 (labelled Figure 2). First, it cuts off at around $400,000 of taxable income, which is roughly the threshold for the top 1 per cent of income earners. Second, it only measures income that appears in a tax return. That is a narrow measure of income. For most taxpayers, taxable income is a reasonable proxy for economic income. For the very wealthy, it is not. Much of their economic income can accrue through unrealised capital gains that are rarely taxed in the year they are earned.

Figure 2 Treasury’s measures of tax rates on income only include income that is lodged in a tax return

Source: Treasury 2026

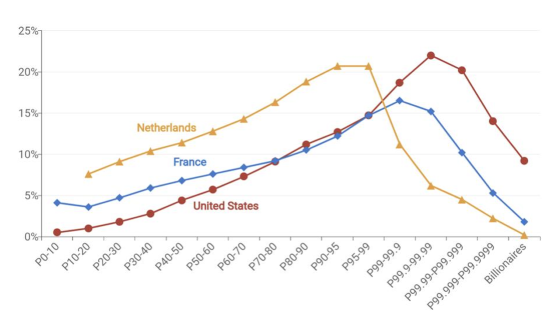

Overseas research shows that once unrealised gains are included, effective tax rates fall sharply at the very top of the distribution (Figure 3). Lumping the 1% together, as Treasury does, masks this dynamic and obscures the effective taxes paid by those within the top 1% of the distribution.

Figure 3 Effective income tax rates on income fall for the extremely wealthy

Effective income tax rates inclusive of unrealised capital gains

Source: Zucman 2024

The reason for this result is straightforward. Ultra-high-net-worth individuals often receive a large share of their economic income through unrealised gains. If they wish to access their income, they can choose to borrow against their assets, rather than sell them. A realisation-based CGT system therefore struggles to tax the very top of the wealth distribution because it only applies when assets are sold.

This creates a targeting problem. It is difficult to tax centi-millionaires and billionaires effectively through a realisation-based CGT system without burdening taxpayers who need to realise gains. The “top 1% of taxpayers” is not a homogenous group. It includes some extremely wealthy individuals, but it also includes surgeons, engineers, lawyers, executives, farmers and small-business owners who may have high taxable income in a particular year. Some of these taxpayers appear in the top 1% because they realise a one-off capital gain.

The proposed reforms therefore fall hardest on people who must realise gains, while doing much less to tax people whose wealth can continue compounding unrealised. That is not a targeted way to reduce inequality. It raises more tax from realisation events but does not adequately target the structural advantages available to the highest-wealth households.

2.4 Deemed CGT disposal at death is a more practical and progressive basebroadening reform

Annual taxation of unrealised capital gains would address indefinite deferral from ultra-high net worth individuals more directly, but would create serious valuation, liquidity and administrative problems. Private businesses, property and other illiquid assets cannot be accurately marked to market each year. Taxpayers could also face substantial liabilities without receiving any cash, including on paper gains that subsequently disappear, requiring complicated rules for loss carry-backs, refunds and payment deferrals. These difficulties have made broad accrual-based systems uncommon and have rightfully generated significant opposition when governments have attempted to introduce them.

A more practical approach would be to adopt features of the Canadian CGT system, where death is treated as a deemed disposal event at market value. This would preserve realisation-based taxation during a person’s lifetime while ensuring that gains cannot be deferred indefinitely and ultimately escape the CGT base. Spousal rollovers and extended payment arrangements for genuinely illiquid estates could address liquidity concerns without permanently forgiving the accrued gain. Similar deemed disposal measures should also be introduced for trusts on a periodic basis (i.e. Canada’s 21-year rule).

2.5 Recommendation

- Phase out negative gearing over a 5-year period for all homes.

- Broaden the CGT tax base by introducing deemed disposal at-death for CGT and periodic deemed disposal on trusts.

3. Investor housing should be taxed more heavily than equities for CGT purposes

Despite the Treasury’s preference for neutral CGT treatment across assets, the proposed tax changes will treat at least one asset class concessionally13: new dwellings. This choice will introduce new complexity with limited additionality and ignores the more central problem when it comes to taxation of property investments. Where economic rents occur in specific asset classes there can be a strong economic efficiency rationale to break tax neutrality and tax rents. In the CGT system, specifically around rents that occur from land uplift, there is a strong case to increase CGT on property, as several other countries already do (i.e. Taiwan, Korea, Israel).

3.1 How are capital gains in the housing sector generated?

Capital gains on housing can arise from two different sources:

- The building – investment in the physical dwelling: bricks, mortar, and fittings.

- The land – the underlying site, the bundle of location-specific amenities and planning rights attached to it.

This distinction matters because it tells us whether the concessions benefit new housing investments or landholding. The evidence points to the latter. In the early 1950s, land at the urban fringe accounted for well under 10 per cent of the value of a typical new house. By the early 1970s, land shares had risen to around 50 per cent of the dwelling’s value.14 Since then, land has become the dominant component of dwelling values in Sydney and other major cities. Decompositions of house values into land and structure components find that by the mid-2010s, roughly two-thirds of the average house value in Sydney was land.15 Rapid price appreciation since then would imply this share has risen further. In other words, the “capital gain” realised when an investment property is sold is predominantly a land gain, not a return to the owner’s investments in the quantity or quality of the physical dwellings on the land.

3.2 Why housing gains are different: land windfalls rather than rewards for effort

For business equity, capital gains more closely resemble a reward for taking on commercial risk, innovating, and creating new products or services. When an investor backs a firm that grows, hires staff and raises productivity, the resulting capital gain reflects genuine value creation. One can reasonably argue that tax relief for such gains encourages socially beneficial risk-taking that expands our productive capacity. By contrast, most long-run gains on residential property – particularly in established urban areas – are not of this character. These gains primarily arise because:

- planning decisions restrict or shape the supply of housing in desirable locations;

- publicly funded infrastructure and services (transport, schools, hospitals, parks) raise the value of nearby land; and

- population growth alongside rising incomes increases competition for a relatively fixed quantity of well-located sites.

Individual owners do not design the transport network, determine migration policy, or set zoning rules. Yet when these factors drive up land prices, the private owner receives a private benefit. Consequently, uplift on land can be taxed at higher rates than appreciating equities, without the same level of economic harm to investment.

3.3 Carve-outs for “new” housing are well-intentioned, but bad housing policy

The proposal recognises the case for non-neutrality but then explicitly breaks it. Negative gearing and CGT carve-outs for “new” housing are a mistake. The problem is simple: these carve-outs do not make construction cheaper. They do not reduce the cost of labour, materials, energy, finance, infrastructure or approvals required to construct a home. To the extent that the concession does affect behaviour, it is likely to be capitalised into higher land or purchase prices for sites that are already viable rather than bring forward new investment in housing.

Other countries have made and reversed similar schemes. France, most notably, subsidised new rental properties through schemes such as Pinel, before abandoning the policies after sustained criticism. The French government’s national auditor on reviewing Pinel found that tax concessions for new rental housing proved costly, failed to decrease rents, disproportionately benefited higher-income investors, and did not create a durable stock of affordable rental housing. Likewise, academic evidence has also found that these schemes inflate land prices, distort the type of housing supplied, and fail to genuinely add to supply.16 17

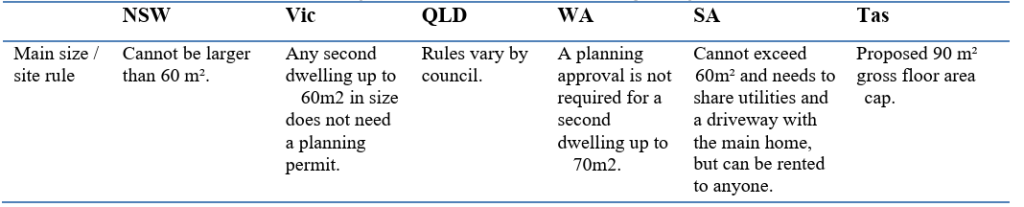

The other problem is that the definition of “new” housing is fraught and the proposed legislation grants too much ministerial discretion in determining which assets receive concessional treatment. This creates uncertainty for investors and also creates a standing invitation for lobbying, and therefore, corruption. It is likely that even if the concession begins with newly constructed dwellings, pressure will grow to include other types of construction that “genuinely add to supply” including, substantially renovated dwellings, knockdown rebuilds, conversions of non-residential property into residential property, granny flats, and extensions. For instance, there is already debate about whether granny flats are included in the new scheme, and what constitutes a granny flat from a tax perspective. Granny flats are inconsistently defined across Australian states (see below). Furthermore, several states already have processes in place to allow the rezoning of granny flats into fully fledged dwellings, which would warrant their consideration as a new dwelling under the proposed CGT changes.

Table 1: There is no nationally consistent definition of granny flat

Source: Australian Broadcasting Corporation 2026

3.4 Suggested options for reforming CGT and negative gearing on investment housing

The tax system should be reorientated to shift taxes off income and onto economic rents. Reducing the CGT discount on residential investment property from 50% to 30% would reduce the relative incentive to speculate on property. This reform would be administratively simple, as it would rely on the existing discount structure and could utilise pre-existing ATO look-through rules for land rich assets.

Likewise, most OECD countries do not allow the full deductibility of investment losses against labour income.18 Ring-fencing investment losses from labour income would remove the artificial incentive to borrow to fund investments, particularly property investments, reducing investor pressure that bids up scarce land. Notably, one study found that the removal of negative gearing could boost homeownership rates by 5.5 percentage points.19

3.5 Recommendation

- Cut the CGT discount on investor housing to 30% and/or introduce a separate property tax regime for land uplift at sale. Use a time-weighted discount to transition to the new scheme.

- Phase out negative gearing for all homes over a 5-year period.

- Do not pursue a new-housing carve-out for either negative gearing or CGT.

- Repurpose revenue to cut personal income tax rates.

4. No other OECD country has a CGT system like Australia’s new inflation indexing scheme

The move to an inflation-indexing model is not well justified. But if the Senate decides to move forward with it, there are design flaws in the proposed system that put us at odds with the handful of OECD countries with an inflation-indexing approach. Despite statements by Treasury First Assistant Secretary Dr Shane Johnson at Budget Estimates that Australia’s inflation indexing system would be consistent with other OECD models, evidence does not bear this out.20 Specifically, Dr Johnson argued that taxing real gains and nominal losses would preserve the system’s integrity – similar to other countries that have inflation indexing – by avoiding people who had made real losses making ‘wash sales’ to create taxable deductions to use against their capital gains. Notwithstanding that Australia already has rules against wash sales,21 the suggestion that Australia’s proposed treatment is consistent with other inflation-indexed systems is not borne out by the comparative evidence.

Only 4 other OECD countries utilise inflation indexation schemes: Turkey, Israel, Mexico and Chile. Most of these countries allow deductions for real losses (Turkey, Mexico and Chile). And both Israel and Mexico tax gains at a lower rate compared to other income. Consequently, these countries either have symmetric CGT systems, and/or limit the penalty on gains by capping CGT rates at lower rates than other income.

Australia’s new indexation scheme does neither and hence will harm risky, productivity enhancing investment. The following section will develop case study examples to explain why each scheme is superior to the proposed Australian version and what could be taken from them.

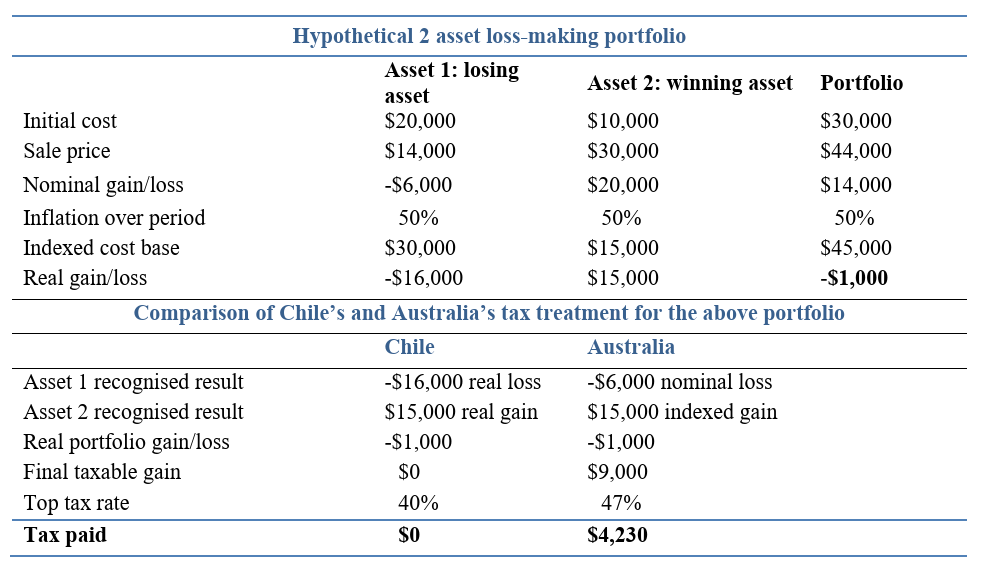

4.1 Australia’s system penalises losses and diversification compared with Chile

Table 2 illustrates how Australia’s proposed system can tax an investor even where the portfolio has made an overall real loss (and assuming the individual has taxable labour income of $200,000). Under Chile’s approach, both gains and losses are measured in real terms, so the $16,000 real loss on Asset 1 fully offsets the $15,000 real gain on Asset 2 and no tax is payable. Australia would instead recognise only the $6,000 nominal loss while taxing the full $15,000 indexed gain, leaving a $9,000 taxable gain despite the portfolio losing $1,000 in real terms.

Indexing losses as well as gains reduces lock-in by allowing investors to dispose of poorly performing assets without forfeiting the inflationary component of their loss, supports risk-taking by ensuring the tax system shares more symmetrically in both successful and unsuccessful outcomes, and encourages diversification by taxing the investor’s net real portfolio return rather than selectively recognising real gains while understating real losses.

Table 2: Two-investment loss-making portfolio – Australia vs Chile

4.2 Israel taxes equity upside more lightly

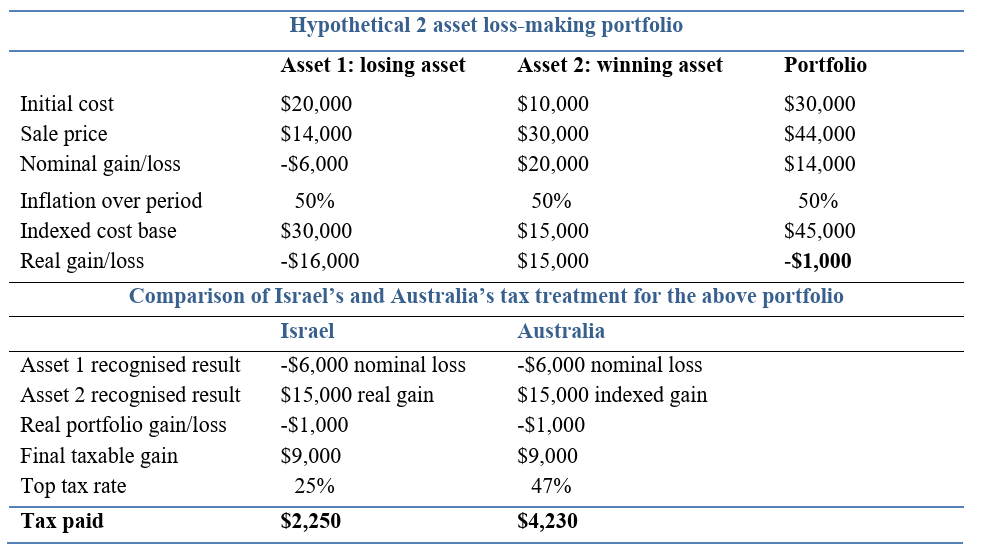

Table 3 illustrates the pragmatic trade-off embodied in Israel’s approach. Like Australia’s proposed model, Israel generally does not index capital losses, meaning that the $16,000 real loss on Asset 1 is recognised as only a $6,000 nominal loss. The investor is consequently taxed on a $9,000 net gain even though the portfolio has lost $1,000 in real terms. However, Israel limits the resulting penalty by generally taxing capital gains on ordinary shareholdings at a flat rate of 25 per cent.

The lower rate reduces the government’s claim on successful investments and therefore partly compensates investors for the restricted recognition of losses. It preserves more of the upside from risky investments, reduces the incentive to retain appreciated assets solely to defer tax, and makes it less costly to sell winners when rebalancing a diversified portfolio. In this example, the Israeli investor pays $2,250 in tax, compared with $4,230 for an Australian investor subject to the 47 per cent top marginal rate. Israel’s system does not achieve the full gain–loss symmetry of Chile’s model, but it avoids combining nominal-only loss relief with taxation of real gains at very high personal income-tax rates.

Table 3: Two-investment loss-making portfolio – Australia vs Israel

4.3 Israel also taxes property uplift more heavily

Israel’s approach also distinguishes between returns from ordinary financial investment and windfall gains arising from the planning system. In addition to the ordinary taxation of gains on real property, Israel imposes an additional levy where a planning decision increases the value of land – for example, through rezoning, approval of additional building rights, a planning variation or permission for a more valuable use.

The levy is equal to 50 per cent of the increase in value attributable specifically to the planning decision. It is therefore not imposed on 50 per cent of the property’s total capital gain. Instead, a valuer compares the property’s value before and after the relevant planning change, with the levy applying to the resulting planning-created uplift. Liability commonly becomes payable when the enhanced rights are realised, such as when the property is sold or developed.

As noted in Section 3, this type of taxation more closely aligns with economic rents in the property sector. A gain arising from successful investment in a business may reflect risk-taking, innovation and productive activity. By contrast, an increase in land value caused by additional development rights is largely created by a public regulatory decision rather than by the landowner’s effort or investment.

4.4 Trade-offs between Chile and Israel’s models

The implicit trade-off between the Chilean and Israeli models concerns tax avoidance and loss harvesting. Chile’s model is theoretically more coherent: by indexing both gains and losses, it makes the tax base broadly neutral with respect to inflation and avoids disproportionately penalising risky investments whose returns are concentrated in a minority of successful assets.

The UK experience, however, demonstrates the integrity risks created when indexation can generate or enlarge deductible losses.22 Before the reforms introduced from November 1993, UK taxpayers could use indexation to produce a deductible capital loss even where an asset had not fallen in nominal value. Such losses could then be crystallised through sale-and-repurchase transactions and used to offset gains on successful investments, without materially changing the investor’s underlying portfolio exposure.

If this tax avoidance strategy cannot be deterred through administrative measures such as wash-sale rules, then Israel’s model represents a more pragmatic compromise to preserve risk-taking. Israel does not provide symmetrical inflation indexation for capital losses, thereby limiting opportunities to manufacture and harvest inflation-generated losses. However, it partly compensates investors for this asymmetry by applying a comparatively low maximum capital-gains tax rate—generally 25 per cent.

4.5 Recommendation

- If pursuing an indexation model, index losses like Chile or cap the top marginal tax rate for capital gains like Israel and Mexico.

- Introduce development pricing to capture rezoning windfalls.23

5. The new temporary and foreign resident tax treatment rules are broken

One final major concern about the move to an inflation-indexing model is its effects on temporary and foreign residents, which appears to be a breach of international taxation norms. Under the proposed rules, an individual will be ineligible for indexation if they were a foreign or temporary resident at any time during the asset’s holding period. Separately, an Australian resident who ceases residency may generally choose whether to recognise the deemed disposal on departure or defer the gain until a later disposal. The interaction of these rules means that an Australian who temporarily becomes a foreign resident may preserve deferral but lose indexation for the asset’s entire holding period. That means the eventual tax bill can be much higher, because inflation is taxed as if it were a real gain, which means it can easily push tax rates over 100% in real terms.

5.1 The residency rule penalises Australians who temporarily leave the country

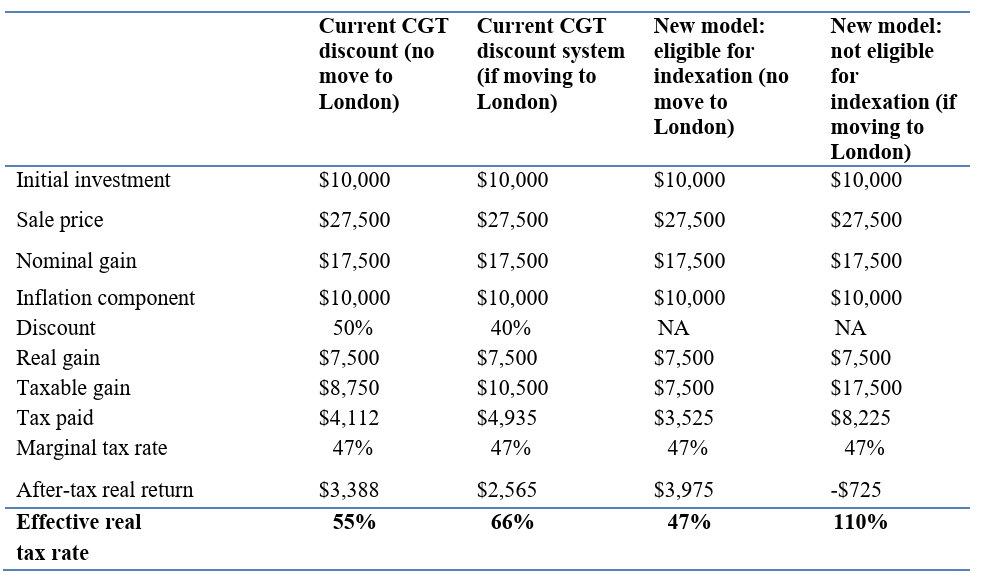

Take the example below of an Australian on the top marginal tax rate who holds an initial $10,000 investment in a CGT liable asset, then becomes tax resident in London for 2 of the 10 years that they hold the asset. They then decide to realise their asset, when their labour income is at $190,000. As shown in the fourth column, it can very easily produce effective tax rates at over 100%. This contrasts with the existing system, where the discount is scaled down as a proportion of time spent overseas (see the second column of Table 4). For instance, when a person has been overseas for 2 of the past 10 years, their discount is reduced by a fifth (i.e. from 50% to 40%).

Table 4: Case study of a person moving to London for 2 years out of 10 on the top tax rate

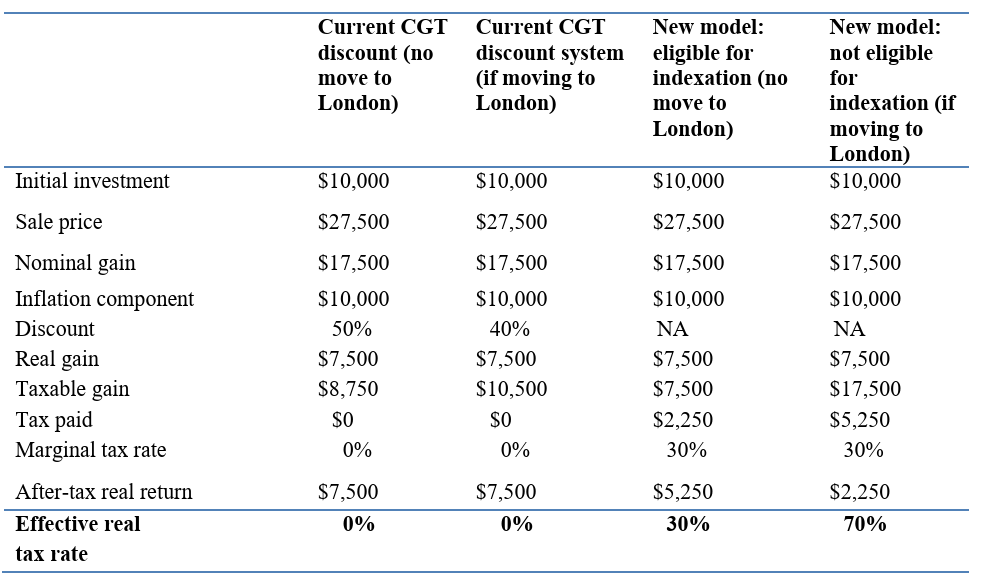

The rules are also punitive for taxpayers with little or no other assessable income. Under the existing system, their gains may fall below the tax-free threshold; under the proposed system, the 30 per cent minimum rate would still apply, as shown in Table 5.

Table 5: Case study of a person moving to London for 2 years out of 10 with no other assessable income when they realise their asset.

5.2 Principles to follow

A fair tax system should apportion tax benefits and liabilities according to the period in which a taxpayer is within the Australian tax system. It should not deny indexation or concessional treatment for an entire holding period merely because a person was a foreign or temporary resident for part of that period. The current CGT discount rules recognise this principle through apportionment in relevant cases. The proposed model’s use of an all-or-nothing rule creates harsh outcomes for Australians who temporarily move overseas, migrants who arrive in Australia with existing assets, temporary residents who later become permanent residents, and returning expatriates. It is, in effect, a tax on mobility.

5.3 Recommendation

- Revert to a proportional model that reflects different periods of residency.

References

- Wilkinson 2026 ↩︎

- Hourani & Perret 2025 ↩︎

- Wilkinson 2026 ↩︎

- Hourani & Perret 2025 ↩︎

- AER 2018 ↩︎

- Bond, Devereux & Klemm 2007 ↩︎

- Hourani & Perret 2025 ↩︎

- ATO 2022 ↩︎

- Wilkinson 2026 ↩︎

- Council of Financial Regulators 2019 ↩︎

- ASX 2023 ↩︎

- Treasurer Jim Chalmers 2026 ↩︎

- The Government has flagged the potential to provide relief for startups, but at this stage nothing concrete has been announced. ↩︎

- Stapledon 2009 ↩︎

- Kendall and Tulip 2018 ↩︎

- Bono & Trannoy 2019 ↩︎

- Daly 2025 ↩︎

- C. Gillitzer 2025 ↩︎

- Cho et al 2017 ↩︎

- Dr Johnson stated that the “rationale for using nominal losses is to preserve that integrity of the tax system, and that is consistent with other countries that have adopted similar arrangements on the taxation of real gains” (Budget Estimates 04/06/2026). ↩︎

- ATO 2024 ↩︎

- UK Parliament 1993 ↩︎

- See Helm and Williams (2026) that explores how to implement how to set-up pricing of development rights. ↩︎