Australia has two infections that compromise our economic health. Their remarkably similar symptoms – fever, delirium, impaired judgement – muddy diagnosis and hamper effective treatment.

Most are familiar with ‘Dutch disease’, where a resource bounty – in Holland’s case off-shore oil and gas production – lifts a country’s exchange rate, makes other activity like manufacturing and agriculture uneconomic and cause great dislocation even while headline GDP and national accounts look rosy.

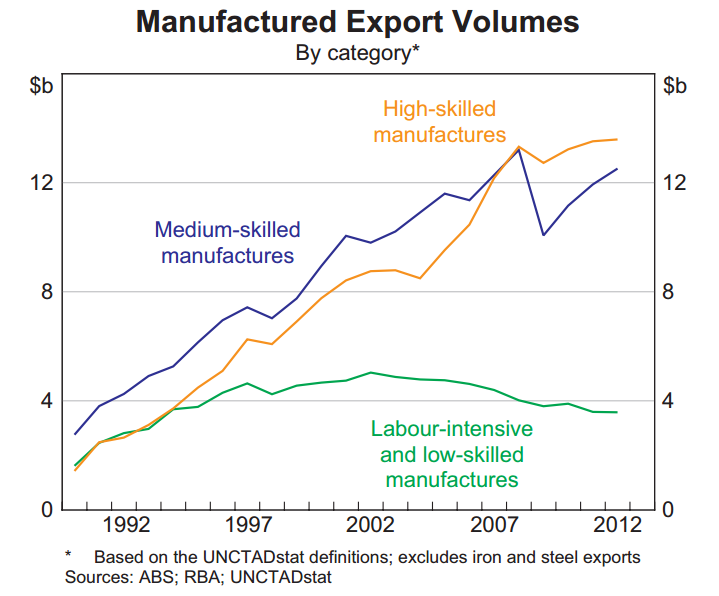

Australia has a dose of this clap. I don’t need to recite the benefits of the mining investment boom that has employed so many trades at premium wages to install major engineering projects at remote sites. These attractive but short lived opportunities and very large in-bound investment amplified the exchange rate pressure from the boom in commodity prices.

Import-competing manufacturing in Australia retired to bed and wasted away. Any local advantage in being close to customers and the high transport costs on imports were not enough protection when the high local currency lifted real wages and local on-costs over these barriers.

What we lost was labor intensive and low-skilled manufactures – metal bashing, plastic moulding and so on. Australia’s high and medium-skilled manufacturing exports show remarkable resilience, yet would benefit mightily from a lower exchange rate.

The masked disease is the ‘Finance Curse’. Dr Andrew Baker of Queen’s University Belfast says:

“It should be noted that the finance curse also relates to the question of global imbalances, because countries with high levels of financial innovation and skilled financial centres can attract financial inflows that produce domestic financial bubbles. Such inflows act as a substitute for poor performance and low wages in other areas of the economy. The resulting economies are therefore prone to sharp reversals, as well as bubbles, which create contagious and paralysing debt pollution and complex negative feedback upon the performance of the wider global economy.

He lists its symptoms as:

• Where financial sector growth raises local prices, particularly the exchange rate, making it harder for alternative tradeable sectors to compete in world markets;

• Brain drain, where higher salaries in finance suck the most skilled and educated people away from other sectors;

• ‘financialisation’, where financial activities take precedence and start to damage genuine productive activities, generating their own endogenous growth including money creation and rent extraction;

• uneven geographical and spatial development, where major global financial services centres concentrate resources, activities, investment and people in a vast urban hub at the expense of underdevelopment and neglect elsewhere;

• rising inequality and social stratification as a small metropolitan elite accumulates vast resources, inflating asset and property bubbles, producing financial instability and making asset ownership difficult for large sections of the population; and

• political capture, where the financial sector becomes disproportionately influential in politics as state resources, policies and institutions are directed towards financial protection and promotion, weakening alternative sectors and creating disincentives for government officials to take corrective action due to easy rents.

Does this sound familiar? I see it fitting the lived Australian experience like a glove.

”For its part, the rise to prominence of macroprudential regulation after the crash of 2008 represents the best endeavour yet to curb the build-up of financial and credit cycles. In this sense MPR is a sticking plaster solution to the finance curse, something that is system-repairing rather than system-transforming. But in some guises the macroprudential lens also wrestles with how the structure and size of the financial system generates instability. The Bank of England’s chief economist, Andy Haldane, refers to the vacuum cleaner effect of finance, sucking resources away from long-term growth enhancing R&D and infrastructure projects. In his visit to SPERI earlier this year, Haldane stated that the purpose of macroprudential regulation was to ‘make finance the servant rather than the master’. Bank for International Settlements research has indicated that banks can start to act as a drag on growth when their balance sheets go above 100% of GDP. Much macroprudential diagnosis does therefore implicitly acknowledge finance curse symptoms and their macroeconomic impacts as the problems to be tackled.

I don’t advocate crushing the finance sector for its sins – though it certainly deserves it. No, the root cause and ultimate solution lie entirely in the hands of government.

The point of infection is government’s addiction to heavy wage taxation and failure to harmlessly tax down economic rents. Wage-earners carry a disproportionate part of the cost of government with income tax, payroll tax and, yes, superannuation tax.

I return, yet again, to the recommendations in Australia’s Future Tax System: introduce two taxes – a land tax and a Resource Super Profits Tax, to fund the removal of 125 dumb taxes we know cause genuine economic harm.

Those untaxed economic rents in land and resources are financialised – borrowed against by individuals and enterprises to increase their reach and grasp.

Mortgaged homeowners get a taste of this in their gearing to magnify land price rises. Negative Gearing – a desperate and risky lunge to escape wage taxation – is a half-step further.

The really big gains fall to finance, which aggregate and nullify the individual gambles, capturing the naturally occurring economic rents to their salaries and shareholders. Our failure to properly identify this second disease imposes great costs on us all. So, let us migrate to a sound and durable economic system that rewards work and enterprise.

Government, reform thyself.