The Business Council of Australia (BCA) has urged the federal government to implement policies that facilitate workers relocating interstate or overseas to where they are needed. From The AFR:

Members of the BCA said the government must invest in infrastructure and housing to make less developed states more attractive to workers.

Companies should also pay incentives to encourage the labour force to move, they say.

“Our fly-in, fly-out concept is very unique to Australia and reflects our cultural mindset that we are just not willing to move for work,” KPMG chairman Peter Nash said. “In the United States you find a much more mobile workforce, and if you want more people to move, you have to build the infrastructure and housing to make it more appealing.”

Ernst & Young managing partner Rob McLeod suggested that bonuses should be linked to whether employees are willing to move. “Business needs to think about linking incentives to mobility: if you are not willing to move, you don’t get as many dollars,” he said.

“You also need to try harder to sell it to workers.”

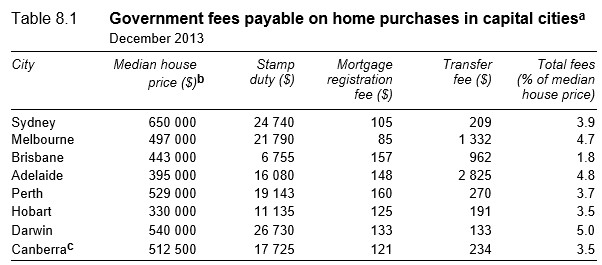

One of the biggest impediments to labour mobility are stamp duties levied on housing transactions. Stamp duties can add tens-of-thousands of dollars to the cost of changing home, leading to fewer transactions and discouraging labour mobility.

Indeed, the Productivity Commission’s (PC) final report on Labour Mobility, released in April noted:

Conveyancing duty (stamp duty) imposes additional costs on property transactions and leads to a lower level of property exchanges than would occur in the absence of the tax…

Various tax arrangements can add to the costs of individuals or firms moving location (such as the stamp duty incurred in property transactions)…

Business SA (sub. 11) consulted with member businesses in South Australian regional areas about impediments to geographic labour mobility. It found that a common concern among members was that ‘potential employees were unwilling to sell their property and purchase another due to the high burden of stamp duty’ (sub. 11, p. 2)…

A 2007–08 survey by the ABS (2009a) found that 26 per cent of households reported that they were unlikely to move in the 12 months following the survey as they were unable to afford the costs associated with moving…

The PC also recommended replacing stamp duties with broad-based land taxes:

Past Commission inquiries have recommended replacing stamp duties with a more efficient form of taxation, such as a broad based land tax, as this will improve flexibility and efficiency in the housing market (PC 2013b). A more flexible housing market will also support geographic labour mobility, allowing more workers to move to areas with better employment opportunities…

RECOMMENDATION 12.2

State and Territory Governments should remove or significantly reduce housing related stamp duties, and increase reliance on more efficient taxes, such as broad based land taxes.

In my view, stamp duties are one of the worst taxes going around. Not only do they hinder labour mobility by discouraging workers from relocating closer to employment. But they also unnecessarily penalise people that move to homes that better suit their needs. Obvious examples include baby boomers downsizing from large family homes and young growing families upsizing to bigger family-friendly homes. Such disincentives inevitably lead to an inefficient use of the housing stock, such as empty nesters occupying large homes with multiple spare bedrooms.

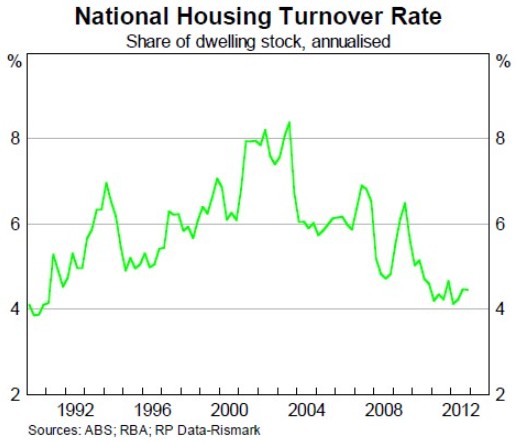

Stamp duties are also highly inequitable. As shown in the below RBA chart, between 4% and 8% of the housing stock is transacted annually. As such, we have a bizarre situation where a small minority of the population are paying taxes that support services for the whole community – all for the privilege of moving to a home that better suits their needs!

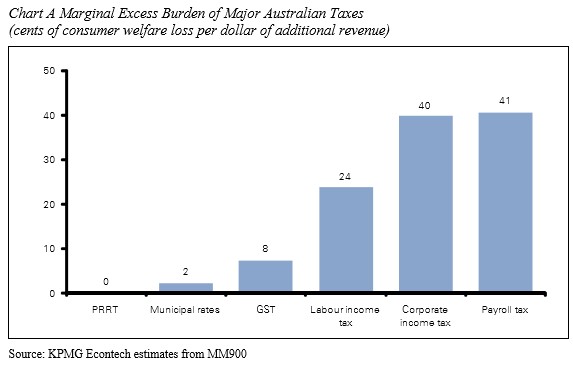

The PC is right to recommend replacing stamp duties with broad-based land value taxes (LVT). Taxes on land are some of the most efficient going around, creating minimal “marginal excess burden” (i.e. a small loss in consumer welfare relative to the net gain in government revenue), according to the Henry Tax Review. This is because they are applied to a tax base that is completely immobile – land (see next chart). By contrast, the Henry Tax Reviewfound the marginal excess burden of stamp duties to be a relatively high at 34%.

As argued previously, there are also broader reasons to endorse the implementation of LVTs in place of stamp duties. First, an LVT would help make infrastructure investments self-funding for governments, since any land value uplift brought about through increased infrastructure investment (e.g. new roads, trains, etc) would be partly captured by the government via increased LVT receipts. Accordingly, governments would be more likely to facilitate development, rather than act to restrict it in a bid to save on infrastructure costs. Second, an LVT would penalise land banking and vagrancy, effectively increasing the supply of land in the process and bringing new homes to market more quickly.

As with any change to the tax system, there are transitional issues that would need to be worked through in shifting from stamp duties to a broad-based LVT.

One concern is that those who recently purchased a property (and paid stamp duty) would be double-taxed via an LVT. A logical solution is to credit all landowners with the amount of stamp duty paid and then deduct the hypothetical land tax they would have paid since the date of purchase.

Another concern is that asset rich, cash poor, retirees could be left with LVT bills they cannot pay, requiring them to sell their homes. A logical solution is to allow these people to accumulate their LVT liability, with the bill payable upon death (via the estate) or once the house is eventually sold (whichever comes first).

The options are there, and for the sake of both efficiency and equity, the federal government should work with the states through COAG to establish a timetable for reform to change the tax mix. The BCA and other business groups should also champion reform by actively making the case for change and placing pressure on both the state and federal governments.

unconventionaleconomist@hotmail.com

www.twitter.com/leithvo