by Philip Soos

Escalating housing costs have, of course, received much attention as both prices and rents increased faster than incomes and inflation over the last decade. In this vein, property research firm RP Data launched a monthly report called Buy vs. Rent, providing a comparison of housing costs across Australia’s suburbs.

Recent results show that in the vast majority of suburbs, buying is relatively more expensive than renting, except in remote or unattractive locations. Four different scenarios of purchasing with a mortgage were analysed for both houses and units: a principal and interest loan on a variable rate mortgage (388 suburbs are cheaper to buy than rent), a variable rate interest only loan (1975), a fixed rate three year PI loan (674) and a three year fixed rate IO loan (2991).

This is out of 5230 suburbs (many were duplicated to maintain a proper comparison between buying and renting for both houses and units). The methodology ignores many costs of ownership: maintenance, council rates, water and sewerage, land tax, body corporate levies, stamp duty, and legal and conveyancing fees. They represent a hefty proportion of the total annual expenses faced by owners that must be met from current income. A more realistic study would at least include an estimate of these costs, though the exclusion of these costs is not always made clear in mass media reporting.

Data from Australia’s largest mortgage broker, AFG, shows most borrowers have standard variable rate loans, with Reserve Bank data indicating 60 per cent of investor and 25 per cent of owner-occupier mortgages are interest-only loans. The IO mortgage choice is predicated on the hope that housing prices will continue to rise. After a set period, typically 10 or 12 years, the mortgage reverts to a standard PI loan. Given that housing prices have increased by 130 per cent between 1996 and 2010, adjusted for inflation and quality, this strategy has worked effectively.

Interestingly, RP Data also calculated an extra 1031 suburbs would be more affordable to purchase if potential owners were willing to pay an additional $50 per week. Mentioning this is decidedly odd, as it appears RP Data is suggesting home ownership is of relatively greater benefit than renting. One could equally ask how many suburbs would become more affordable if tenants were willing to pay an extra $50 per week in rent.

RP Data has repeatedly claimed that Australian house prices are based upon fundamental metrics (intrinsic value) and is not experiencing a bubble. Yet the report provides some evidence to suggest a confirmation of overvaluation in the residential real estate sector, that is, the market price of property is significantly greater than future rents capitalised. Figure 1 shows the long term trend of Australia’s price to rent ratio.

![]()

Although the ratio in 2007 comprises the second-highest peak in its 131-year history, the post-WWII peak should be discounted on the basis of the government releasing war-era price controls (prices were not market-determined). More recently, the ratio has increased by 64 per cent from trough to peak (1997-2007), though falling housing prices and rising rents in the last two years have resulted in a moderate decrease in the ratio.

The Economist has an interactive graphic that explores the housing metrics of many Western countries. Where a bubble cannot be denied – US, Spain and Ireland – the price to rent ratio rose significantly as the numerator (housing prices) increased but the denominator (rents) remained steady. Other countries experiencing a housing bubble but yet to visibly burst – UK, Canada and Australia – are clearly identifiable by their historically high ratios.

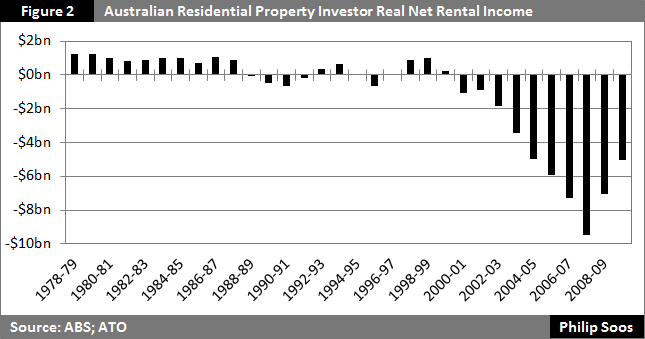

Investors in the residential property market have based their decisions upon expecting future growth in capital values rather than rents. In 2008, economist Gerard Minackargued that property had a price to earnings ratio of above 30 based upon gross yields. This ratio jumps to over 100 when property expenses are factored in (net yields), indicating a significant mismatch between housing prices and rents. Figure 2 illustrates that, on aggregate, investors since 2000 have been making a zero net yield, along with substantial net rental income losses.

Conventional economic theory stipulates that, in an efficient property market, the all-in risk and tax-adjusted cost of purchasing a property should equal the cost of renting it. In economic jargon, this is the ‘user cost scenario,’ essentially the effective cost of securing housing services. If buying is dearer than renting, then supposedly rational individuals will change their preference by selling, taking the profit, and renting, driving down housing prices until the cost of buying equals the cost of renting.

The divergence between prices and rents in the US before the housing market collapsed confused mainstream economists who could not explain why prices were sky-high but rents merely tracked inflation. According to neoclassical economic theory, this should not occur. A Federal Reserve study suggested that the ratio is a good indicator of property valuation but when the analysis concluded that the US appeared to be experiencing a bubble in 2004, excuses were made to dismiss the idea.

The usual conjectures were that information asymmetries, impeded dwelling construction and high transaction costs were causing imperfections in property markets. Obviously, it was not these factors causing the divergence; this was the largest debt-driven housing bubble in US history. Economist Dean Baker argued correctly in 2002 that the divergence between housing prices and rents was the result of a bubble in prices.

Those who take an interest in the property market know a wide gulf exists between prices and rents, indicating there is something amiss. One explanation is property ownership attracts a significant, qualitative premium which is difficult to verify quantitatively. Another is that the strong growth in capital values since 1996 has resulted in a large appreciation rate factored into housing prices.

The likely reason behind the increase in the ratio is debt-financed speculation. This serves to drive up housing prices but does not influence rental incomes. Rental incomes are anchored to wages, so workers/tenants cannot indefinitely rent above their capacity to pay. Also, competition in the rental market (tenants’ threat of leaving) ensures that rents do not rise unjustifiably out of control. On the other hand, capital values are determined by banks’ willingness to extend credit to home owners and investors, limited only by lending regulations (if banks choose to observe them) and borrowers’ ability to service the mortgage repayments.

The recorded history of Australia’s real estate sector shows one bubble after another in both the commercial and residential property markets: the 1880s, 1920s, mid-1970s, early 1980s, late 1980s and today. It is not surprising that the ratio has increased given the run-up in housing prices and net rental income losses. The ratio serves as one of many indicators to determine possible overvaluation in the real estate sector. It comprises a valuable metric and thus should not be ignored.

Philip Soos is a researcher at Deakin University’s School of International and Political Studies.

Top stuff, Philip Soos!