by Philip Soos

For those interested in the Australian residential property market, below are a collection of figures illustrating long-term trends. Housing prices and land values are compared to a basket of fundamental metrics. Australians are fortunate because much data on real estate and financial markets are publically available, going into depth not seen in other countries.

Comparing housing prices to inflation is one of the more common indicators in property market analysis. If the trend is fairly even over time, then there is no indication that people are favouring housing relative to other goods and services. On the other hand, if there is a wide divergence between housing prices and inflation, this tells us that people are considering housing to be relatively more important. Interestingly, every rise in real prices has led to a downturn, with the one exception of 1961-1964.

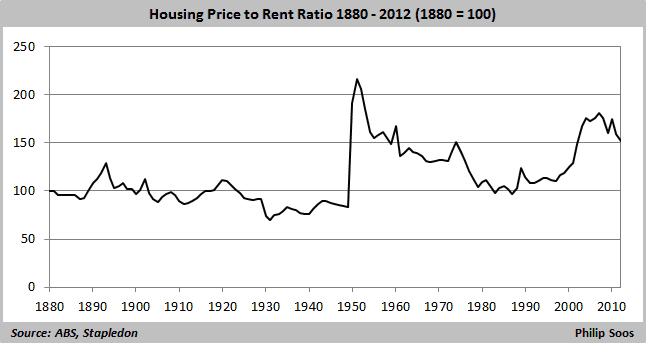

Another popular method of determining property valuation is comparing housing prices to rents. In a fairly efficient market, the costs of buying and renting should closely match each other, though due to factors such as taxes, risks, and interest rates, it is unlikely that costs will equal. Since the post-WWII boom, the ratio has unevenly decreased. Upswings in the ratio suggest the presence of a bubble: the mid-1970s, early 80s, late 80s, and today.

As with inflation and rents, housing prices have also outstripped incomes as well. Unfortunately, the Australian Bureau of Statistics does not provide a long-term median household disposable income series, so the denominator is derived by dividing aggregate real gross household income by the number of occupied households on an annual basis. This results in an unusually high HDI as averages are typically greater than medians, and is further amplified as the HDI is stacked with artefacts like superannuation which cannot be drawn upon to finance debt repayments. While the outcome is a rather low ratio, it keeps in line with that developed in Stapledon’s 2012 housing paper and shows a substantial increase from 1996 onwards. A more realistic median measure would result in a higher ratio, and the latest Demographia report shows it to be so.

<a

It is easy to see the major cause of the Great Depression: a deflating land bubble, centred in the commercial property market. Every major rise in the ratio has resulted in a downturn, correlating with, and arguably, causing the economic recessions of the mid-70s, early 80s, and early 90s. The ratio has doubled from the trough in 1996 through to the peak in 2010. The substantial rise in the ratio during the late 1970s was likely due to an anomaly in splicing multiple land value series together, though part of the rise is justifiable because of a residential bubble.

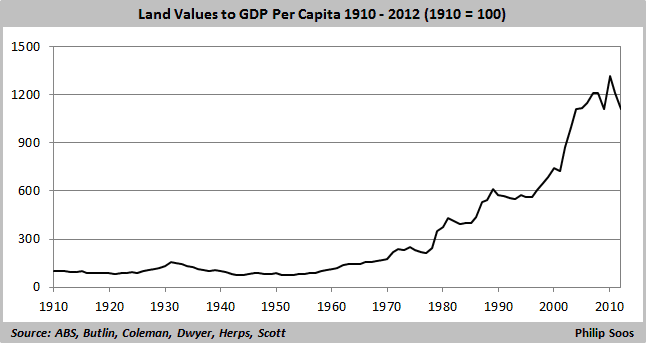

The same story emerges when land values are compared with GDP per capita, which is arguably a better fundamental metric than GDP itself. As with the previous figure, the ratio has doubled during the same time period.

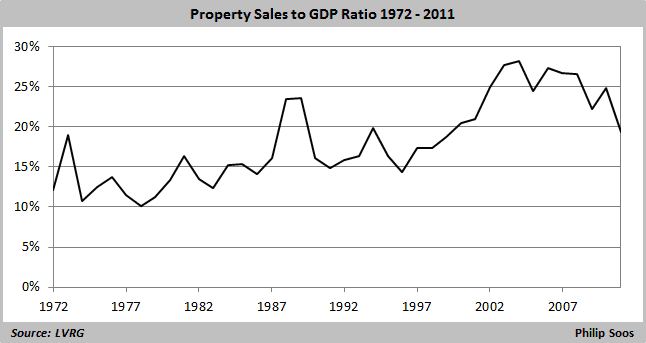

The Kavanagh-Putland Index measures the ratio of property sales to GDP. This metric is considered useful because in times of speculative fervour, investors flip properties to one another, increasing the total value of sales on an annual basis. When real estate markets tank, sales inevitably fall as potential buyers stand by the wayside waiting for further price falls. The ratio peaked in 2004 after housing prices jumped in the years previous.

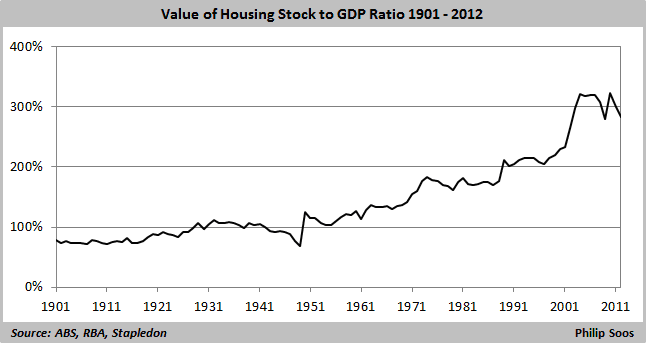

The value of housing stock to GDP has likewise moved in the same direction as house prices to inflation and land values to GDP. It is the land component rather than the dwellings that has increased in value over GDP.

The primary determinant of the boom-bust cycle in the land market is availability of credit/debt used to speculate on rising capital values of real estate. While data on private debt goes back to 1861, aggregate land values only begin in 1910. Debt peaked in 1893, driving a colossal commercial land bubble that burst, causing the worst depression in Australia’s recorded history. Again the same occurred during the 1920s, with the same result. It took until the 1970s for the debt cycle to assert itself once again, with one boom and bust after another. Debt reached the highest peak on record in 2008, driving the largest land boom on record.

Unsurprisingly, the cause for the massive rise in housing prices and land values, along with net rental income losses, is the colossal increase in household debt, primarily composed of mortgage debt. It has more than quadrupled since 1988, rapidly accelerating during the 1990s and 2000s. The ratio peaked in 2010 as did housing prices, which is clearly no coincidence.

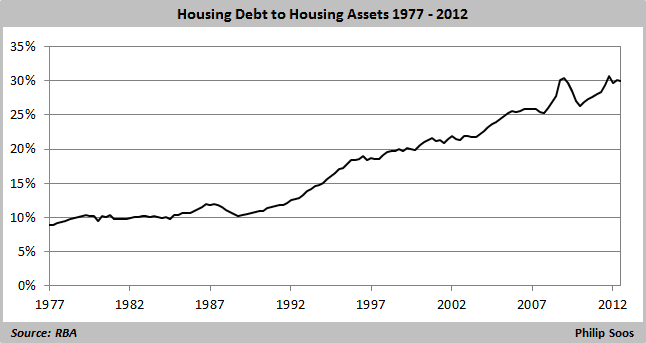

As household debt has climbed, so too has debt as a percentage of household assets. The ratio will rise as housing prices continue to soften. It has tripled from 1990 through to 2008 before the GFC, falling and then resuming its upward climb.

The same has occurred with housing debt to disposable income, tripling over the same time period.

Despite very high interest rates during the early 1990s, the ratio peaked in 2008 due to the staggering debt load of households, even at lower interest rates. It is no surprise that this ratio closely matches the net income losses experienced by property investors as shown in the next figure.

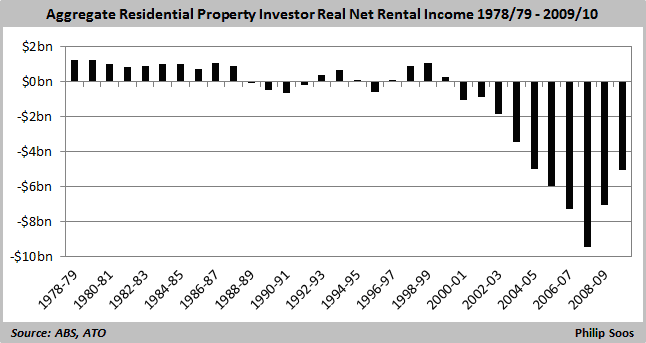

Perhaps the most telling of all data are investors’ ability to finance the debt and routine expenses on their residential properties. In the midst of the late 1980s commercial land bubble, an element of residential speculation caused real housing prices to increase, most notably in Sydney and Perth. Speculators suffered income losses from 1988/89 to 1991/92 while seeking capital gains. The market later stabilised before making the largest net income losses from 2000 onwards, signifying a zero net yield and massive residential bubble.

The obvious cause of these losses is due to the rise in interest repayments rather than running expenses, which have remained stable at around 50 per cent of gross rental income. Interest repayments peaked in 2008, driven by higher interest rates before the GFC hit.

Not only are investment properties overvalued, the entire residential stock is. The vast majority of properties are owner-occupied, at almost 70 per cent. Since 2004, all owners on aggregate have been running net income losses which do not bode well for them once capital values stop increasing.

Once again, it is interest repayments that are the cause of the income losses. A slight uptick in expenses during the 2000s surely didn’t help, but has since then fallen back to its long-run average.

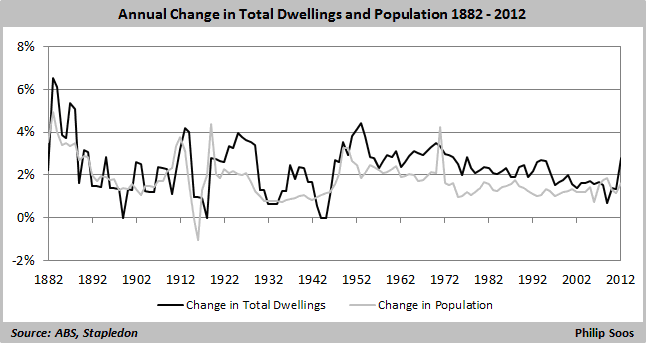

Despite the best efforts of the National Housing Supply Council and the FIRE sector (finance, insurance and real estate) to spruik a housing shortage, the long-term trends show dwelling growth has consistently outpaced population growth since WWII. From 2008 to 2009, the trend reversed temporarily.

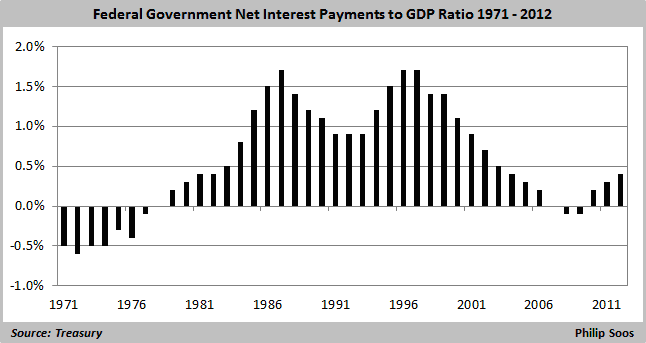

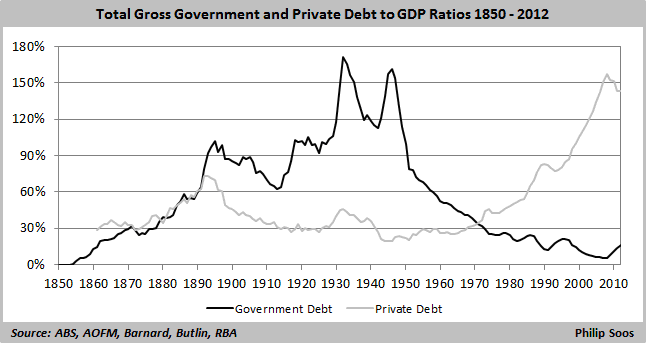

Perhaps the only positive factor is the government’s relatively low position of gross debt to GDP. The fashionable idea often repeated these days is that rising public debt poses a risk to the economy has little substance in reality. Compared to the pre-WWII era, the governments of today are a picture of fiscal responsibility and prudence, with the rise in taxation revenue helping to offset the need for using debt. In the event of a substantial and prolonged downturn in the economy, the federal and state governments are well-placed to debt-spend.

A better measure of government debt is net rather than gross debt, and even better is the net rather than gross interest repayment burden, expressed as a percentage of GDP. What matters for countries that have high levels of government debt is how great the net interest repayment burden is. This is what separates the US and Japan – countries with a relatively high level of government debt – with the basket-case PIIGS nations (Portugal, Italy, Ireland, Greece and Spain). Australia is currently situated in an excellent position, and even if the government debt to GDP ratio were to rise, this does not necessarily translate into higher net interest repayments if the Reserve Bank further cut interest rates from already historical lows and purchased government bonds.

Increases in the government debt to GDP ratio are typically due to two occurrences: world wars (1914 to 1918 and 1939 to 1945) and responses to economic downturns caused by private debt-financed speculation: the 1890s, 1930s, mid-1970s, early 1980s, early 1990s and the GFC in 2008. The rise in the ratio before the 1890s was due to colonial government mass construction of public infrastructure. It is obvious to see which type of debt today presents an overwhelming macro risk to the economy. Government debt will inevitably rise to counter private debt-deleveraging but it is very unlikely that political parties will engage in the necessary and timely expansion needed to ward off the adverse effects of debt-deflation.

In conclusion, the data presented should provide more than enough evidence to suggest that Australia’s residential property market (specifically land market) is vastly overvalued, driven by debt-financed speculation and the relative non-taxation of land rent. While land bubbles have been a continual feature of the Australian economy, what separates this cycle is the relative enormity of the boom in both land values and private debt. A smaller private debt to GDP ratio during the 1880s and 1920s was enough to produce two devastating depressions, including a number of recessions during the mid-1970s, early 1980s and early 1990s.

The question is often asked why housing prices are so high. Instead, the real question is to ask why prices are so low. The banking and financial system is ready to lend absurd amounts of debt to the willing army of ‘greater fools’, and has constructed an elaborate chain from mortgage brokers’ offices through to the business development managers at the banks in order to commit extensive fraud by manipulating loan application forms. This is the ‘six degrees of separation’ Denise Brailey has uncovered. Consequently, the only determinant that prevents the banks from lending more credit is debtors’ ability to finance repayments out of current income. Only when it becomes difficult to finance repayments will the housing and land markets finally capitulate.

It is often claimed “this time is different”. It certainly is, but not for the reasons usually given: Australia has not experienced a land bubble of this magnitude in its history. Seven in ten adults own property, solvency of the FIRE sector is dependent upon ever-increasing capital values and the governments’ addiction to housing-related tax revenue and votes, its none-too-surprising bubble deniers have been out in full force, asserting housing prices are based upon fundamental valuations. Also unsurprising is that all bubble deniers have conflicts of interest, and in an age of the secular equivalent of religious fanaticism and greed, facts and history are conveniently dispensed down the memory hole.

The only option left to policymakers is to continually kick the can down the road, hoping the bust does not occur on their watch. The result, as seen with the Rudd government’s additional First Home Owner’s Boost, was precisely that. This intervention restarted the debt machine, re-inflating housing and land prices to a new, higher peak in 2010. The overarching private debt bubble, which began in 1964, will likely come to an end once and for all when the government runs out of fuel to throw on the fire.

Philip Soos is a researcher at Deakin University’s School of International and Political Studies.

Unfortunately, none of this data is much use if you live in Perth. After a 15 year absence, in the 1 year I’ve been back housing prices and rentals have gone up about 18% (from my own foot-slogging research). Is this a bubble? Of course! But no mention is made anywhere by any “expert” about the real cause.

To wit: Untold Billions in hot money from wealthy, individual investors (India/China/S.E.Asia) pouring in from overseas to lock up this market. These people are not on the radar of Forbes, The Economist or the WSJ simply because they have no idea how to quantify such private wealth. So they do what all opinion leaders do who control the status quo; they ignore them and continue to mumble about interest rates and other stats they CAN access.

Which is why we get this mystifying leap upwards in prices when data suggests a popping should be happening. Perth’s bubble will go on for another 2-3 years, most likely. It will become one of the largest percentage-increase bubbles in history if current rates of increase are any guide.

Australia’s population growth is also continuing to increase at a greater number every year (with more than 2/3rds attributable to immigration) which will also contribute to the desire for speculation in the Australian market.

But this is unravelling quickly as a whole host of other considerations come into play. Extreme weather, lack of economic diversity, lack of and depth to our economy, lack of consideration for Australia’s energy security, whole-sale sell-off of the majority of Australia’s primary wealth (ironically, to pay for the rapid population growth policies) are coming together in a perfect storm.

You’d have to be a sucker to buy into Australia’s real estate market but in China alone there are some 560,000 millionaires being courted, there’s bound to be no shortage of suckers.

I agree with your comments hidflect. I have been living in Perth for the last 7 months and despair almost at what it costs to put a roof over my head. Despite being able to obtain well paid permanent employment, buying a house is pretty much out of the question. Maybe on an interest only loan but that’s just expensive rent unless there are prospects of significant capital gains. Every house I look at in my price range is ‘under contract’ with buyers offering 10% – 15% more than the listed sale price just to secure a property and agents “stopping writing after 8 offers to buy”. I don’t know how long and how far can this go. I’m just too conservative to take the risk and worry that the bubble will eventually pop. It won’t of course while WA attracts 1,500 new migrants a week and while SE Asia continues to boom. My instincts tell me that current price levels are now structurally imbedded and there is no going back to the old days of 3 x a single person’s average earnings to buy a house. It’s now at least 6 x and these metrics I’m afraid are here to stay. I’d like to stay in Perth but it is a place for the young and talented who can afford to take on the commitments as well-paid young couples. Everyones’s a winner – banks, governments getting votes from happy owner voters, the real estate industry and the various markets for consumption items paid for by people feeling wealthy. The marginalised of us eventually admit defeat and move elsewhere. Perhaps Perth and Sydney are becoming the new Monaco’s?

I was going to email the author and ask if he had read Henry George, Progress and Poverty, and low and behold, I scroll down to the bottom of the website and there is a list of links about him! Obviously Prosper is inspired by him.

Great you have read the master, Dean! His writing still stands the test of time.