Australia’s economy is dominated by sectors which derive significant revenue from “economic rents” – or unearned income. These include land, natural resources, legal privileges granted by intellectual property rights, and highly restricted and regulated industries. The top three by Gross Added Value are land ownership, mining, and finance.

We contend that as returns to ownership of a scarce resource, or supernormal profits, are generated by uncompetitive market structures, we should be careful when we add them to measures of gross value added to the economy.

The difference goes unreported and is not well understood. When a mining company is granted the right to extract a non-renewable resource, it is essentially being granted permission to realise a windfall by selling a public asset. When a landlord charges a rent, they are not adding to the supply of land. Indeed the whole concept of trading property among ourselves as a value adding activity is spurious. Similarly, the ‘value add’ generated by the financial sector – which is not producing anything so much as greasing the wheels.

And economic rents respond very differently to taxation having little to no deadweight loss. Understanding this difference is crucial if we are to liberate the productive sector, and shift the tax burden onto economic rents.

By failing to differentiate unearned and earned incomes, for example the company tax rate is the same across the board, our current tax system favours industries that receive significant unearned income, but penalises competitive industries that do not enjoy these benefits.

Prosper first attempted to quantify unearned income in our Total Resource Rents Report (2013), and we also considered the longer term trends of unearned income (from land) in our Trickle-Up Economics Report (2018).

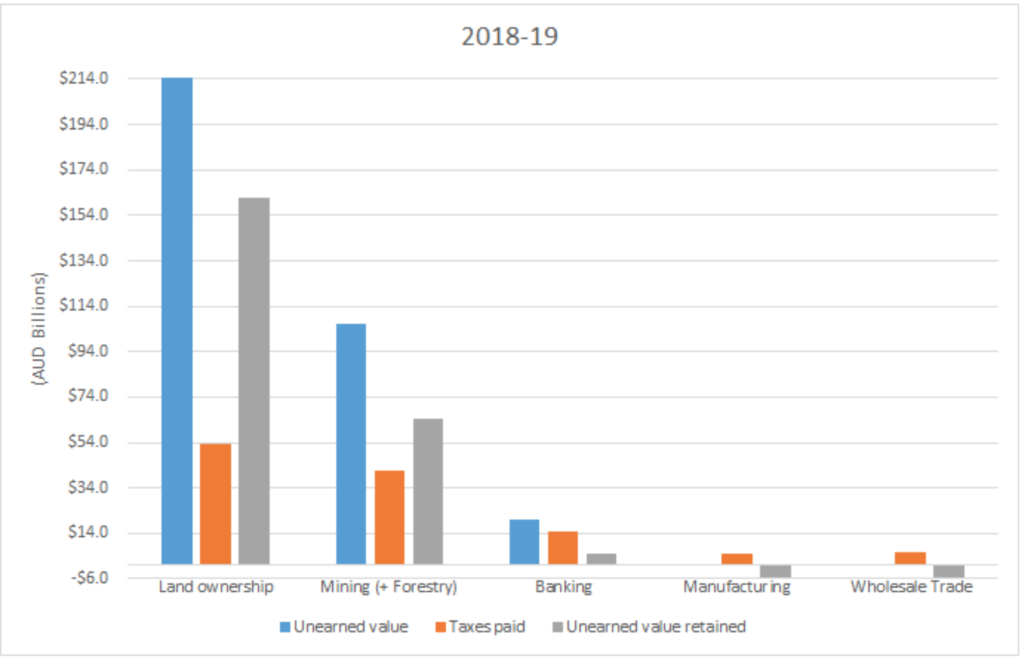

We recently analysed estimates of unearned incomes for the 2018-19 financial year by sector, and compared this with how much company tax they paid. A long-run analysis would be preferred, and will be considered in future.

Sectors that have significant unearned incomes do pay a lot of tax, but when accounting for how much unearned income they receive, they come out well ahead.

Banks interestingly paid most of their unearned income in tax, but still retained a bit, even after the banking levy was introduced. The method I used built off Cameron Murray’s estimates in Game of Mates, however arguably this is a conservative measure as it does not factor in rents accruing to entities exempt from “money-client rules” (i.e. can create credit).

Mining (which includes negligible forestry due to OECD data limitations), also contributes significant taxes. However this appears only over 1 year, a longer term analysis would likely show many years gone by where relatively little tax was paid. It is likely that the Resource Super Profits Tax (mining tax) from over 10 years ago would’ve closed this gap significantly.

In the case of land, total revenues from rates, land taxes, and stamp duties dwarfs the total tax base – we collect about 25% of the annual rental income value. Land ownership in any technical sense does not add value, rather it is the value extracted by owners for access to the use of land.

To obtain this estimate I used ABS 5204.049 (for residential land rent), and ABS 5204.061 alongside Valuer General Victoria estimates of NAV and CIV (to find non-residential yields).

The methodology I have used for land looks at the recurrent rental value for land only. It is important to note that this excludes capital gains.

In a recent paper by Kumhof et al. it was highlighted that there is a significant difference between a land tax base that only looks at the annual rental value, and one that taxes the asset price of land (which land taxes in Australia generally do). In my discussions with Kumhof, I came to the (embarrassingly obvious) realisation that asset prices also capitalise in expected future capital gains income into the price.

What this means is, land value is determined not only by how much rent you think you can get from the land, but also by how much you think it will go up in value over time (who would’ve thought!). So when we use a land tax on an asset price i.e. pay 1% of your land’s value, we are also taxing unrealised capital gains. The faster land value grows, the more the tax collects. This means the tax base I have used in this graph significantly underestimates the amount of unearned income that goes to land.

If we assumed a general growth of land income that matched GDP growth (~2.5% on average post-GFC), capital gains would add another $144.2bn (67% of the rental income). This is probably still conservative, given average residential land growth is much greater than 2.5% (although may largely be driven by temporary yield compression). These numbers would make the graph look more like this:

The problem is we don’t know how much on average capital gains are being taxed through the income tax system. Owner-occupiers don’t pay at all, and investors usually get 50% tax free thanks to the capital gains tax discount. It’s unlikely it changes this graph much.

Meanwhile we see productive and competitive industries like manufacturing and wholesale trade continue to pay significant taxes with no unearned income to help them. This is dwarfed by landowners, miners, and banks who are getting a free ride even after paying tax.

Maybe we should shift to some better taxes?

Hi Jesse,

How might a tax on land affect the expected growth in land prices and subsequently the unearned income and associated tax revenue as discussed in the last graph? This probably requires a degree of assumption particularly if modelling over time. Also, although possibly not directly relevant to your analysis, if one of the objectives is to analyse what effect introducing a tax system of this nature would have on land/asset prices then how much effect would the year of introduction have with respect to our understanding of the land price cycle? Levying a tax on land in 2012 may be expected to have less impact on suppressing land prices at that time compared to levying that tax now or in the next few years?

Hi Matt,

I think it depends on the wider tax settings and if there is any tax reform coinciding with land tax.

The first thing would be land taxes in principle shouldn’t alter the growth in Gross land rent or capital gains. However it captures a share of that, which means initially expectations would readjust in the short-run to account for the socialised proportion of land rent and capitalise gains, and the final private amount leftover would then capitalise into land prices. For example, if land was taxed so 50% of the land rental value and 50% of the (unrealised) capital gains were socialised, then the land price would fall by 50%. However subsequent growth in land rents and the associated expected capital gains should still be proportional i.e. the total growth would be split 50/50, but because the asset price is also halved the growth rate remains the same for the private owner.

For example if you had a $100 of land that produces a total return of 5% p.a. and land taxes initially resulted in it falling to $50, an annual gross growth in before tax value of 5% wouldn’t change. The land would still produce a return of $5, but $2.50 would go to the state and $2.50 would go to the private owner. $2.50 of $50 asset value still being a 5% return for the private owner and thus the growth in market land values in general remains unchanged.

So in the long-run I would not expect land taxes to affect growth in capitalised land values, it would instead be an adjustment process. Cutting other taxes in addition to this, would then have further knock on effects.

As for the timing of introducing a land tax, in theory there would be variation in the effect on asset values depending on the expectation of capital gains. Given during land booms a lot of the price escalation comes from anticipation of higher prices (future capital gains capitalising into land prices), land tax would be more potent in deflating asset values because it would stall those asset bubbles. Whereas if expectations of capital gains are low, values are more reflective of land rent and so there is less speculative value to be suppressed. Increasing land tax rates as interest rates fell would’ve also likely offset the subsequent boom by keeping people’s discount rate or yield for land constant.

Michael Kumhof (2IC at the Bank of England) et. al recently put out a paper modelling this sort of thing actually. I think it would be of great interest to you:

https://iceanet.org/wp-content/uploads/2022/01/Kumhof.pdf

https://imf.webex.com/recordingservice/sites/imf/recording/f831c37e6010103a97fc00505681fa31/playback

It looks at the long-run impacts of these reforms holding everything else constant. It appears land prices in most scenarios fall substantially relative to the status quo or “trend”. But again, I suspect these are merely transition effects. I don’t think they would reduce the growth rate in land values once everything has filtered through. Eventually in the model land prices stabilise and reach an equilibrium, indicating that there is not a constant drag on the growth in land value.

N.B. Land tax could also have an interesting effect of altering perceived highest and best use for the site over time, and how people value land. You can imagine a scenario where the most optimistic/speculative buyer anticipates large capital gains; a higher a high land tax would mean this optimism becomes heavily discounted by higher expected tax payments; relative to another buyer who might not anticipate such growth but be more focused on the value the land can produce today from its income and so anticipates lower tax payments. This comes from Cameron Murray’s research on options theory for development, where higher taxes discount the value of delaying (in favour of more dense future development) and bring forward development timing decisions to acting on what can be produced profitably today. It would also likely reduce the price of raw, undeveloped land, while boosting the value of already developed and productive land (which yields higher returns once taxes on earnings are reduced) – further increasing incentives to develop/redevelop. This is looked at in our paper here: https://osf.io/mxg3j/